So, you’re thinking about saving for retirement.

You’ve probably heard of multiple options you can invest in, from Traditional IRA’s to 401(k)s, but what is a Roth IRA? How is it different from a regular IRA? And how do you set one up?

Continue reading to find out everything you need to know about Roth IRAs and how you can start investing with one today!

What is a Roth IRA?

A Roth IRA is an individual retirement account (IRA) that includes qualified tax-free withdrawals. This means that the money you put into it has already been taxed. When you cash it out in retirement, there are no taxes on it. The money you see is what you get. For low-wage earners like college-aged individuals just starting to think about retirement, a Roth is one of your best options. This is because you will likely be taxed at the lowest rate of your life when you are in this age group.

How is it Different From A Traditional IRA?

The key difference in a Roth compared to a Traditional IRA is how they are taxed. In a Traditional IRA, pre-taxed money gets funneled into the account automatically from your paycheck. This allows for more money to go into your account upfront, letting it grow faster. When you withdraw these funds in retirement, however, that is when they get taxed.

IRAs can be utilized by anyone with earned income, no matter how much they earn in a given year.

How is it Different From Other Retirement Accounts Like a 401(k)?

401(k)s are retirement plans only offered by your employer, whereas a Roth IRA is something you contribute to on your own. In theory, you can have both of these retirement plans over the course of your life. 401(k)s are pre-tax like a Traditional IRA, meaning they go straight from your paycheck to your retirement fund. You determine what percentage of your paycheck goes toward your 401(k). Employers typically offer a 401(k) match, where they will put a certain percentage into your retirement account as well if you decide to contribute that amount or more yourself. This is a great benefit to take advantage of, as it is money you never had going toward your retirement.

The money in your 401(k) isn’t taxed until you withdraw it in retirement. The contribution limits are much higher than a Roth IRA, being $19,500 if you’re under age 50 and $26,000 if you’re over 50 years old.

Including the employer match, the total contributions cap at $58,000 if you’re under 50 and $64,500 if you’re age 50 or older. Due to the fact that you deduct the contribution from your paycheck, your taxable income is reduced, saving you money during tax season.

What Are The Rules of a Roth IRA?

To use a Roth IRA, there are a few stipulations to follow:

- You can’t use one if you make over a certain dollar amount. In 2021, the figures are $140,000 or more a year if you file your taxes as single or over $208,000 for married couples.

- Yearly contributions are capped at $6000 as of 2021 ($7000 for those 50 are older) This figure can increase periodically.

- You can’t withdraw gains without penalty until you are 59 ½ years old.

- In addition to the age requirement, the account must be established for five years from the time it was first funded in order to be a qualified distribution of earnings.

- You can only contribute earned income in a Roth IRA.

- You can always withdraw your own contributions from your Roth IRA at any time with no penalty. Withdrawals automatically come from your contributions first so there’s no risk of getting penalized on earnings until all contributions have been removed.

- The account holder can maintain the Roth IRA indefinitely; there are no required minimum distributions (RMDs) during their lifetime, as there is with 401(k)s and traditional IRAs.

- A way to withdraw earnings prior to the age requirement is if the assets are used toward the purchase of the owner’s first home. However this amount is limited to only $10,000 per lifetime.

- Another way for a qualified withdrawal is if it occurs after the Roth IRA holder becomes disabled or if the earnings are distributed to the beneficiary of the Roth IRA holder after the Roth IRA holder’s death.

How Do I Set One Up?

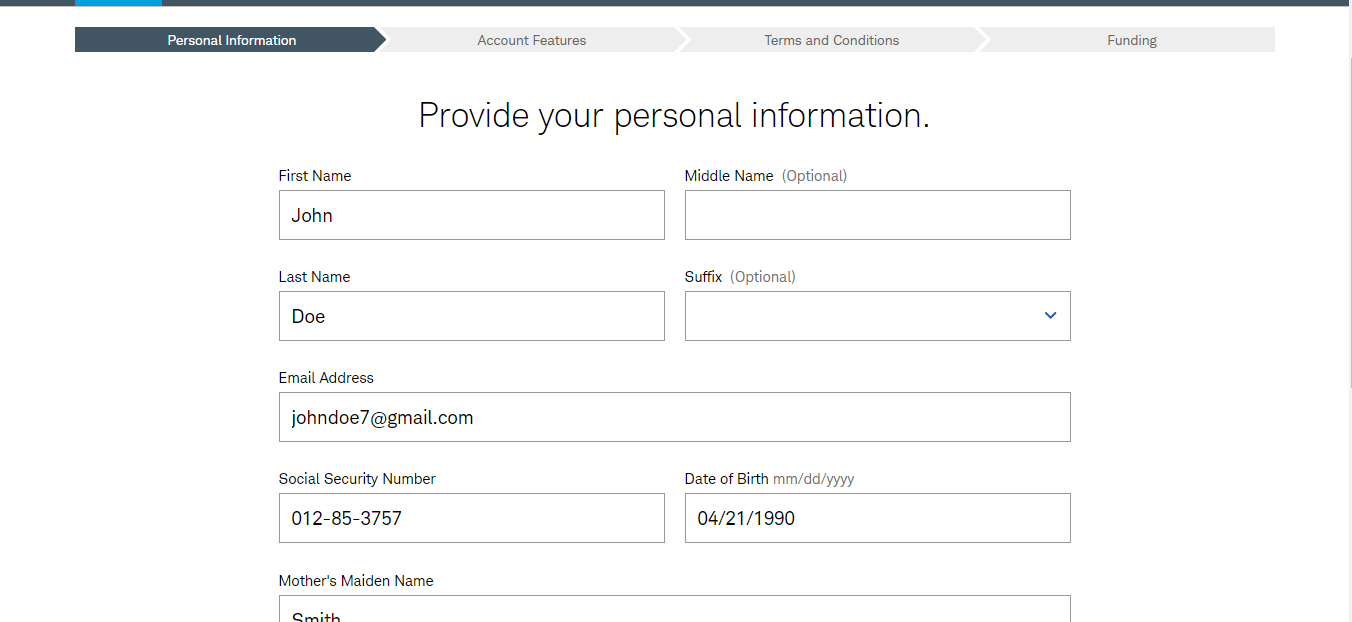

Using a brokerage service such as Charles Schwab, Vanguard, or Fidelity, you can set one up in as little as 15 minutes. For example, if you wanted to set up your account through Schwab, visit their website. From there, just follow the directions and fill in the necessary information. You’ll need to know information like your social security number and what your yearly income is.

Create an account or log in to get started.

You’ll fill out your information before reading over the features of the account, along with the terms and conditions.

Lastly, you’ll add your banking information in order to fund your Roth.

Once your Roth IRA is funded, you’ll click on the “Trade” button to start investing. Determine whether you want to invest in stocks, ETFs, or Mutual Funds and enter in the ticker symbol. Decide how much of your money you want to invest in a certain fund and click “review order.”

Once you review your order and confirm it, you’ve officially started investing and saving for your retirement!

Final Notes

A Roth IRA is a great tool to save for retirement while not having to worry about taxes later in life. Considering the relatively low contribution limit, try to max it out to have the most retirement savings possible over the long term.

Are you going to open a Roth IRA right now? Any questions on what to do next? Let me know in the comments!